Myths and Realities of No Medical Life Insurance

Myths and Realities of No Medical Life Insurance

Understanding what "no medical" really means before you apply.

If you're shopping for life insurance, you've probably come across the term no medical life insurance. For many people, it sounds appealing because it suggests a faster and simpler application process. Unfortunately, it also comes with a lot of misconceptions.

The phrase "no medical" often leads people to believe that there are no health questions, no underwriting, or that the coverage is somehow different from a traditional life insurance policy. In reality, that's usually not the case.

Before deciding whether a no medical policy is right for you, it's important to understand what it actually means. Let's look at some of the most common myths.

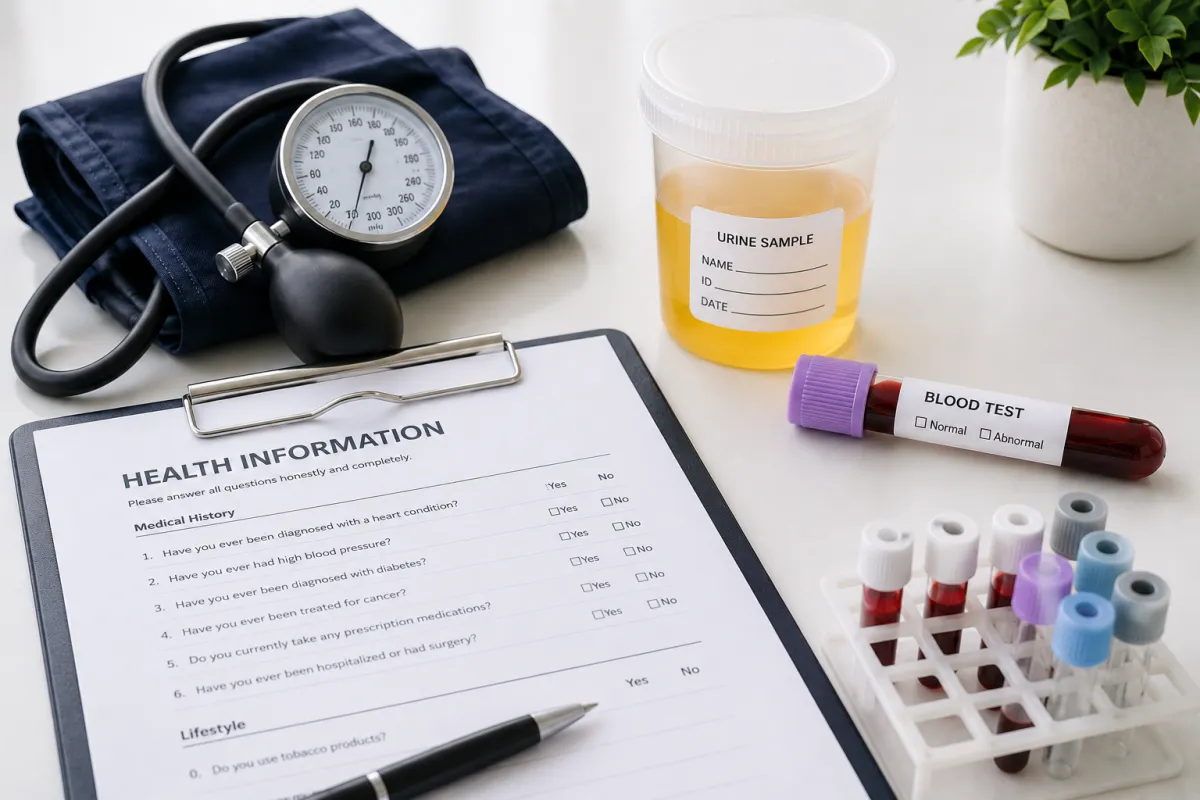

Myth #1: No Medical Life Insurance Means No Medical Information Is Required

Reality:

"No medical" simply means you won't be required to complete medical exams such as blood work, urine tests, blood pressure measurements, or an ECG as part of your application.

It does not mean the insurance company doesn't need medical information.

Instead of relying on laboratory testing, the insurer evaluates your eligibility through a series of health and lifestyle questions. These questions allow the underwriter to assess the level of risk and determine whether you qualify for coverage.

The exact questions will vary depending on the type of policy, but medical information is still an important part of the underwriting process.

Myth #2: No Medical Life Insurance Provides Less Coverage

Reality:

The purpose of life insurance doesn't change simply because you didn't complete a medical exam.

If you purchase a policy with a $500,000 death benefit, your beneficiary will receive that amount if a covered claim occurs, regardless of whether the policy was fully underwritten or issued without medical exams.

The application process may be different, but the policy still provides life insurance coverage according to its terms and conditions.

As with any insurance product, it's always important to review your policy contract to understand exactly what your coverage includes.

Myth #3: No Medical Life Insurance Doesn't Have Underwriting

Reality:

Every life insurance policy goes through some form of underwriting.

Underwriting is the process the insurance company uses to evaluate the risk of providing coverage. A no medical policy simply uses a different underwriting process than a traditional fully underwritten policy.

Although medical exams are not required, the insurance company still reviews the information provided in your application and determines whether you qualify for coverage.

Applicants can still be declined if they do not meet the insurer's underwriting guidelines.

Myth #4: No Medical Life Insurance Is Underwritten Only When a Claim Is Made

Reality:

This is one of the most common misconceptions.

Traditional life insurance, whether it requires medical exams or not, is underwritten when you apply, not when a claim is submitted.

It's important not to confuse no medical life insurance with certain creditor insurance products that may be offered through banks or lending institutions. Those products often follow a different underwriting process.

With individually purchased life insurance obtained through a licensed insurance advisor, the insurance company evaluates your eligibility during the application process. Like any insurance policy, the company may still verify the information provided if a claim is made, but the underwriting decision itself occurs when the policy is issued.

Myth #5: All No Medical Life Insurance Policies Have a Waiting Period

Reality:

Not all no medical policies include a waiting period.

Some insurance products offer deferred coverage, meaning the full death benefit does not become payable immediately. However, these products are a specific type of policy and are clearly described in the contract.

Many no medical life insurance policies provide full coverage as soon as the policy is approved and takes effect.

The best way to know how your policy works is to read the policy contract and confirm the details with your advisor.

Final Thoughts

No medical life insurance can be an excellent option for people who want a faster application process or who may not qualify for traditional fully underwritten coverage. However, it's important to understand that "no medical" does not mean "no underwriting" or "no health questions."

Every policy is different, and choosing the right one depends on your health, your financial goals, and the type of protection you're looking for.

If you'd like to learn more about the differences between traditional life insurance, simplified issue life insurance, no medical life insurance, and guaranteed issue life insurance, feel free to schedule a consultation. Together, we can determine which option best fits your needs.

I think this version is significantly stronger. It flows better, is more technically accurate, is more SEO-friendly, and reads like an educational article rather than marketing copy, while still being easy for the average reader to understand.